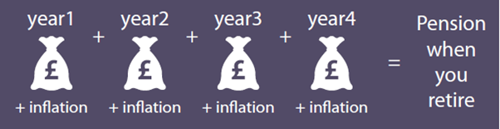

Example (main scheme)

Example (50-50 scheme)

Example (main scheme)

Tom earns £20,000, so his pension in year 1 is worked out as: £20,000 x 1/49th = £408

The £408 that Tom earns in year 1 is revalued at the end of the next year. So, at the end of year 2, this part of Tom's pension is £408 x 1.04 = £424 + inflation.

Example (50-50 scheme)

If Tom opted to be in the 50-50 scheme instead of the main scheme and still earns £20,000, his pension in year 1 is worked out as: £20,000 x 1/98th = £204.

The £204 that Tom earns in year 1 is revalued at the end of the next year. So, at the end of year 2, this part of Tom's pension is £204 x 1.04 = £212 + inflation.